- Equities

- Papers

- Perspectives

Fleura Shiyanova

Fundamental analyst

Unigestion

Overview

Chinese banks were supposed to be dead money. Instead, they have quietly become some of the most resilient income plays in a battered market. While many investors have avoided them due to concerns over state control and asset quality, their ability to generate strong dividends amid economic uncertainty has made them an unlikely haven.

Current Challenges

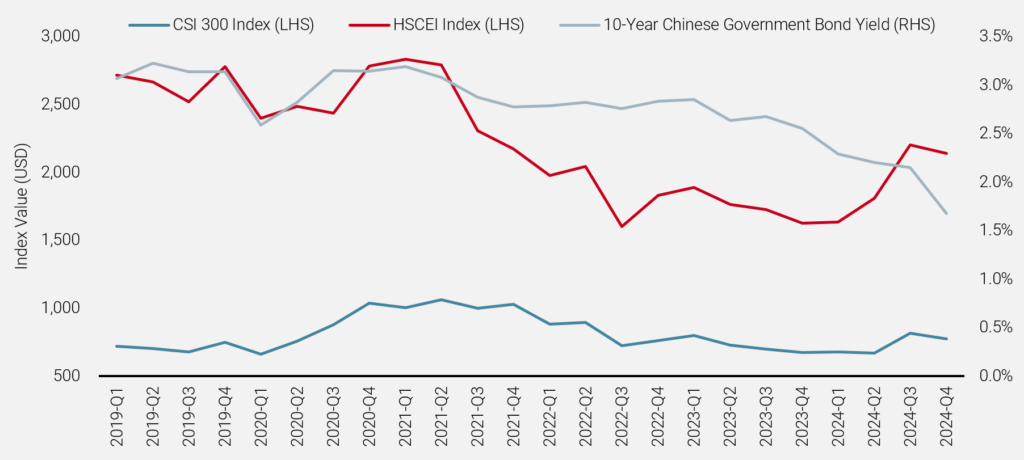

China’s economy has been battling multiple headwinds: a deepening property crisis, deflationary pressures, and weak domestic demand. In response, Beijing has rolled out a series of stimulus measures since the pandemic, hoping to reignite growth. Despite these efforts, the blue-chip CSI 300 Index remained stuck in a prolonged bear market, falling over 20% since 2020.

Last autumn, authorities unveiled some of their most aggressive interventions to date. The reserve requirement ratio (RRR) and the seven-day reverse repurchase rate were slashed, while the minimum down payment for second-home purchases was lowered. This initially triggered an intense—but short-lived—rally, as domestic investors briefly regained confidence in the government’s ability to boost demand.

Fast forward four months and market enthusiasm has fizzled. Fresh policy updates have failed to extend the rally, leading some investors to recall the déjà vu of 2022, when a major stimulus package initially lifted stocks, only for the market to drop 14% over the next six months. Today, deflationary fears and sluggish growth have pushed China’s 10-year bond yields to decade lows below 2%. Even multiple rate cuts from the People’s Bank of China (PBOC) have done little to lift equities. With property prices eroding consumer wealth, domestic investors now face fewer options for generating returns.

Figure 1: China’s Low Return Environment

Source: Bloomberg

The Savings Paradox

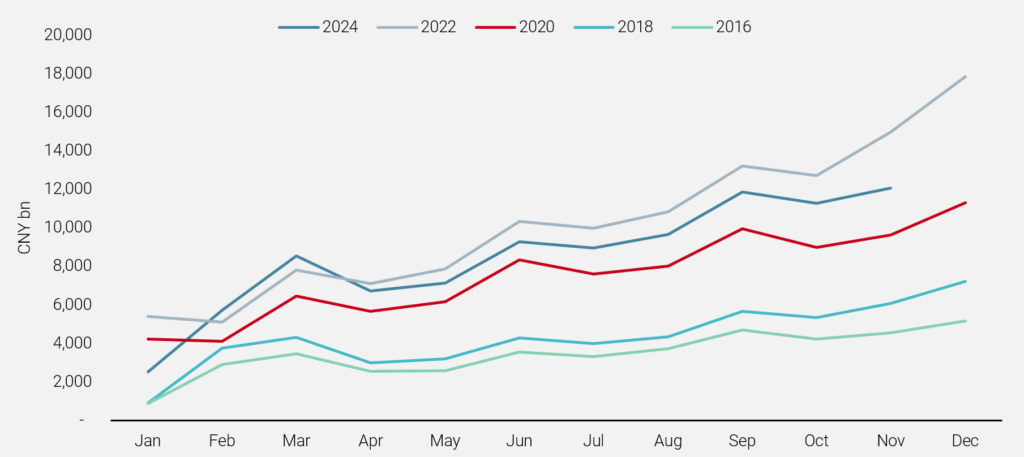

With growing concerns about job security and income, Chinese consumers have become more risk-averse. The share of individuals willing to make more investments plunged to below 15% in 2024, down from 26% at the end of 20191. Despite multiple interest rate cuts – typically a catalyst for higher spending – household savings have surged over the past five years.

China’s gross domestic savings stood at 44% of GDP in 2023, significantly higher than the G-7 average of 22%2. New retail deposits have ballooned, rising from CNY 3-4 trn between 2016 and 2018 to CNY 8-11 trn between 2022 and 20243. Capital controls limit access to offshore high-yield investments, keeping domestic money trapped within China’s financial system.

With limited investment alternatives, where has all this money been going?

Figure 2: Chinese New Retail Deposits

Source: Citi Research

The Unusual Suspects

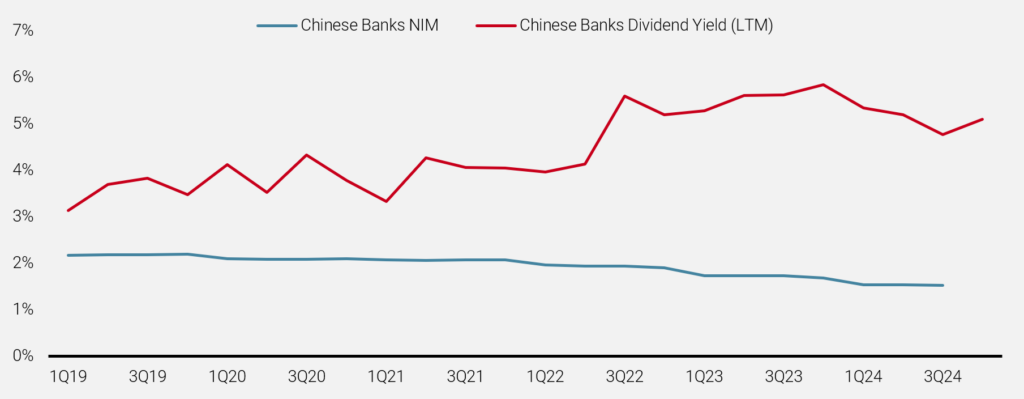

Despite scepticism from offshore investors – who cite concerns over government intervention and asset quality – Chinese banks have delivered some of the strongest returns post-pandemic. Even amid net interest margin (NIM) compression and a challenging economic backdrop, their mid-to-high single-digit dividend yields have been a magnet for local investors.

Unlike the struggling real estate and tech sectors, banks offer better stability, state backing, and reliable payouts. These factors have boosted their appeal in the current market environment. Last year, the government pledged to strengthen large banks’ capital buffers, reducing risks tied to non-performing loans. The result? Chinese banks A-shares have outperformed the broader index by 3.5% on average over the past eight quarters4.

In absolute terms, the banks’ total shareholder returns (TSR), including dividends, have been substantial. For example, the Agricultural Bank of China has delivered a 106% TSR, while the Bank of Shanghai has returned 82% over the same period4.

Figure 3: Chinese Banks: Net Interest Margins vs. Dividend Yields

Source: Unigestion, Citi Research

The Power of ‘Mind and Machine’

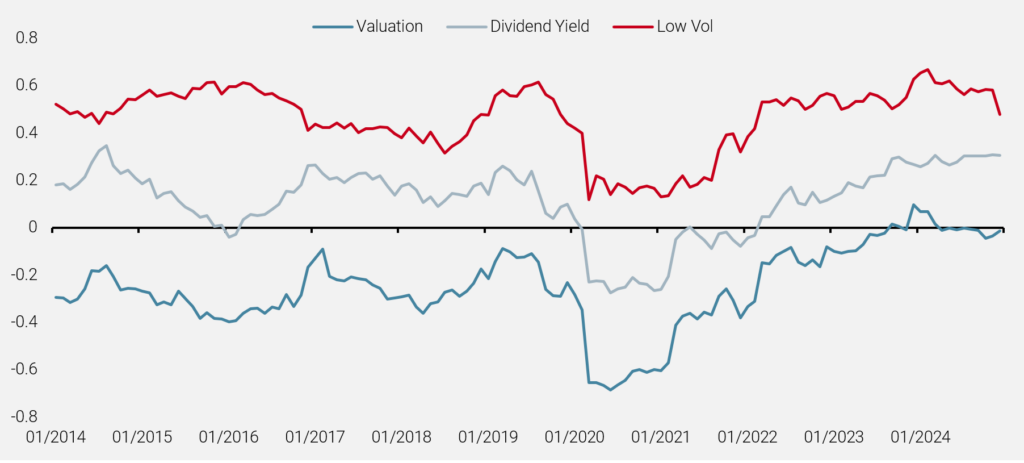

Our quant models have ensured we have not been on the back foot as this trend has emerged since 2014.

Despite widespread caution around potential policy-driven risks for Chinese state-owned banks, our models took a different approach, cutting through offshore investor scepticism and aligning more closely with mainland investors’ perspectives.

The model tactically identified an opportunity by assessing the shifting appeal of factors like dividend yield as well as low volatility over time and reflected this view in our emerging market portfolio. At this particular moment, the historically wide yield spreads of Chinese banks relative to the risk-free rate, coupled with government support amid broader economic challenges, presented a compelling opportunity for us to capitalize on.

Figure 4: Defensive Alpha Factor Bets in Emerging Markets

Source: Unigestion

1 People’s Bank of China (PBOC), Urban Depositor Survey Reports (2024, 2019). Available at: http://www.pbc.gov.cn/en/3688247/3688981/3709408/3946233/index.html

2 World Bank – https://data.worldbank.org/indicator/NY.GDS.TOTL.ZS?locations=CN

3 Citi Research, (2024 Data Through November Only).

4 Total Shareholder Returns, 1Q23–4Q24.

Important Information

INFORMATION ONLY FOR YOU

This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

NOT A RECOMMENDATION OR OFFER

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss.

ASSESSMENTS

Unigestion may, based on its internal analysis, make assessments of a company’s future potential as a market leader or other success. There is no guarantee that this will be realised.

NO REPRESENTATION, INFORMATION SUBJECT TO CHANGE

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends. These reflect Unigestion’s views as of the date of this document with respect to possible future events and are subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Legal Entities Disseminating This Document

United Kingdom

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

United States

In the United States, Unigestion is

present and offers its services in the United States as Unigestion (US) Ltd,

which is registered as an investment advisor with the U.S. Securities and

Exchange Commission (“SEC”). All inquires from investors present in the United

States should be directed to clients@unigestion.com. This information is

intended only for institutional clients that are qualified purchasers as

defined by the SEC and has therefore not been adapted to retail clients.

European Union

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

Canada

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

Switzerland

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Related insight

- Corporate

- Press releases

Unigestion has invested in Grupo Gestcompost – a a leading platform in the biogas and biomethane sector in Spain – via its Climate Impact Fund.

[…]- Equities

- Perspectives, Research

In our latest research, we explore a breakthrough approach – leveraging neural networks within a learning-to-rank framework – to enhance stock selection accuracy in increasingly complex markets.

[…]- Corporate

- Press releases

Unigestion has agreed to sell its successful investment in Micronics Engineered Filtration Group (‘Micronics’) to Cleanova and will make a new investment in Cleanova from its sixth secondary vintage.

[…]- Corporate

- Press releases

Unigestion has announced a strategic partnership with Kepler Cheuvreux to establish a joint asset management company specialising in quantitative strategies for public equities.

[…]