- Private equity

- Papers

- Perspectives

Paul Newsome

Head of Investment Solutions

Private Equity

- Investment and exit activity is down.

- Data shows first time managers outperform in market troughs.

- 2023 could be one of the most interesting and attractive vintage years in the last decade.

Dear investors

While 2022 ended with a surge in investment activity, 2023 has begun with a whimper. Driven by continued macro uncertainty around increasing interest rates, untamed inflation and questionable growth, private equity managers have largely slowed down their investment pace. Investment activity was less than half that of the first quarter of 2022. Meanwhile, exit activity was down by the same proportion, albeit off an already low base. This steady decline in exit activity will continue to encourage certain investors to solve their liquidity issues through the secondary market. Finally, while fundraising was actually 18% higher than the same quarter last year, it continues to be dominated by the mega cap funds: one fund accounted for over 25% of the total amount raised. Indeed, with at least 10 mega cap managers targeting fundraises of USD 15bn or greater this year, it will be increasingly difficult for both established and emerging mid-market managers to fight for investors’ allocations. For those happy few who have dry powder in the mid-market, 2023 has all the ingredients to be one of the most attractive vintages of the last decade.

Investments Down, Exits Down

The global aggregate value of private equity deals closed during Q1 2023 was EUR 177bn, 52% down on the same quarter last year[1]. This decline was seen across all regions with North America (-49%), Europe (-50%) and APAC (-60%) down by similar levels.

Possibly driven by a recent fall in fundraising in the mid-market, investment activity in mid-market companies (defined as deals with an enterprise value of less than EUR 500m) was down by 56% compared to 48% for large companies.

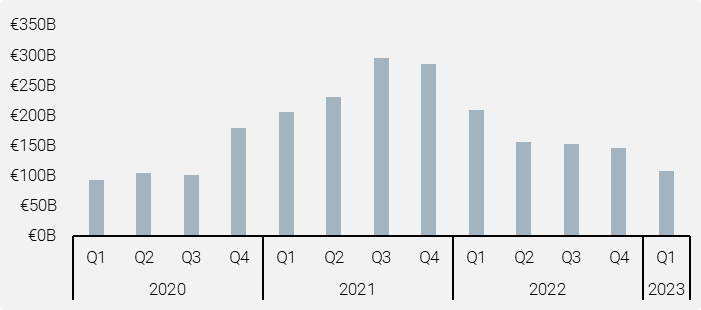

Meanwhile, exit activity showed similar declines. The global aggregate value of exits was EUR 108bn, a decrease of 49% on the same quarter last year. This decline was also uniform across regions with North America (-44%), Europe (-51%) and APAC (-63%) all down. This has now been a relatively consistent trend for the last four quarters, with each quarter being close to 50% down from the same quarter a year ago.

Figure 1: Exit Activity

Source: Pitchbook, April 2023

Fundraising in Q1, at USD 69bn, was 18% higher than the same quarter in 2022. However, more than half of this came from five mega cap funds, suggesting that small and mid-market funds continue to have a difficult time. According to Preqin, there are over 1,000 buyout managers in the market raising an aggregate of close to USD 760bn. Thus, it remains a daunting task for fund managers to convince investors to allocate to their funds, given current fundraising pace.

Furthermore, the market remains bifurcated between the well-established blue-chip names who can raise multiple billions in a matter of months and smaller managers who are taking up to two years to raise, or finalising on smaller than anticipated funds. For example, in April 2023, Genstar raised USD 13.4bn for its Fund XI in a first and final close.

While it is often seen as the comfortable choice for investors to invest with large, household names, data shows that during previous market troughs, it has been the first-time fund managers who have outperformed established managers. There are likely various reasons for this: (1) less capital is raised at the smaller end of the market during difficult periods, leading to less competition for deals, (2) first time managers do not have the burden of needing to fight fires across large existing portfolios, and (3) lesser-known managers are highly motivated to deliver decent returns to investors, while established managers would rather take low risk, low return bets in a more difficult environment.

Figure 2: First-Time vs Non-First-Time Funds

Source: Preqin. Data as at 31 December 2022

In our latest emerging manager programme we have made three commitments in the last two quarters which highlight the attractiveness of backing first or second time funds. We outline two of them below.

In Q4 2022, we committed to Nordic Alpha Partners II. Nordic Alpha is a growth investor in the Nordics, specialising in scaling high potential sustainable hardware technology companies that are addressing the green transformation. Shortly after our commitment, we co-invested in Spirii, an electric vehicle charging infrastructure provider. With over 100% annual revenue growth, the company has quickly become one of the leading EV charging companies in the Nordics and has now launched into Germany. Nordic Alpha and Unigestion were able to invest in this company at a valuation significantly below comparable valuations of its peers.

In Q1 2023, we committed to the Achieve Edtech Buyout Fund, which seeks to invest in software or tech-enabled services companies that facilitate learning. The team at Achieve Partners has worked together since 2016 investing in, operating, and advising EdTech companies, and has deep sector knowledge and expertise, as well as a compelling track record.

Prior to committing to the fund, Unigestion co-invested in MasteryPrep in Q4 2022, a tech-enabled education company that partners with schools and districts to help underperforming students score better on state exams (ACT, SAT, PSAT, TSIA2). MasteryPrep has grown to serve 400+ school accounts mainly in low-income areas within the Southeastern USA. Importantly, Achieve Partners and Unigestion were able to acquire this company at a highly attractive valuation, even though the company is experiencing strong revenue growth.

In this environment, we continue to see attractive secondary dealflow. In March 2023, we closed a direct secondary investment with Charterhouse in Funecap, the largest European funeral services and crematoria business, operating in France, Italy, the Netherlands, Germany, Belgium, and Switzerland. This deal has allowed Charterhouse to roll its investment from a predecessor fund to its current fund. Funecap has downside resilience due to high barriers to entry, long-term demographic trends, pricing power and a leading position as a value-for-money player. The company is expected to continue its successful roll-up consolidation strategy in the fragmented European funeral services market and strengthen its position in adjacent offerings (e.g. insurance).

We are excited about the opportunities that are arising in this environment. In addition, despite the overall slowdown in exit activity, we are working on a number of attractive exits across our direct and secondaries portfolios. We look forward to reporting on these in the coming quarters.

The Investor’s Dilemma

March 2023 might very well be remembered for its tumultuous banking events. Around mid-month, the US Federal Reserve announced an emergency bank term funding program after the sudden collapse of California’s Silicon Valley Bank (SVB) and New York’s Signature Bank. This was followed by a steep drop in Credit Suisse’s share price which, given it was facing imminent failure, was sold to its Swiss rival UBS for CHF 3bn in a government-brokered takeover.

The mood on both sides of the Atlantic was to keep raising policy rates, justified by the ECB and Fed’s resolute battle against inflation, while signaling they could slow upcoming hikes as the banking turmoil is expected to act as a drag on credit growth. This comes in an environment where bank lending standards are already tightening – another headwind for growth.

Like many investors, our first priority was to undertake an in-depth evaluation of our portfolios, assessing our own direct holdings and banking arrangements. We also ascertained the exposure of our fund managers in Europe and the US. Following this evaluation, we confirmed that (i) the exposure to SVB or Credit Suisse is limited, and (ii) there has been no adverse impact on any of our private equity portfolios.

However, while the global banking system is not under the same acute stress as in March, we do not believe that the topic of systematic risk in the regulated and non-regulated banking system is behind us. The effects of rapidly rising interest rates may not yet be fully baked in and, given that central banks remain focused on fighting inflation, further rate rises are likely.

We believe that it is therefore prudent to map and monitor counterparty risk across all of our portfolios on an ongoing basis. This will allow us to react swiftly in the event of any future banking, or other financial crisis.

In the aftermath of this confidence crisis, private equity and venture capital investment activity will likely remain subdued. As a direct implication of SVB collapsing, lending for technology and healthcare companies, mainly venture to growth stage in the US, will become harder and more expensive.

There will be secondary effects and it is not yet clear how this will play out. For example, how resilient will the less-regulated private lending market be? In addition, it is quite reasonable for lenders to increase their credit risk margins in the context of the higher volatility and uncertainty. Hence, we should expect that overall lending costs will experience a significant uplift.

However, for experienced investors, the current environment has the ingredients to make 2023 one of the most interesting and attractive vintage years in the last decade. What will be the most appealing opportunities? Here are some ideas:

Companies expected to be the market leaders of tomorrow. We define these as companies that are leaders in their niche, have strong financial profiles, together with predictable growth from a thematic tailwind and robust balance sheets to invest in organic or acquisitive growth. Returns to investors will thus come from growth and margin improvement rather than leverage. Such companies are found in the mid-market and, in this environment, can be acquired at highly attractive prices.

Entrepreneurs looking to partner. It has likely been decades since entrepreneurs have been confronted with so many moving parts in this “new normal” environment. Just think of the rapid evolution of technology, geopolitics, unstable supply chains, cybersecurity, the climate challenge, inflation, interest rates, FX volatility and ESG. They may prefer to tackle those transformation opportunities with a partner rather than carrying them out on their own. Private equity will excel as the partner of choice, bringing the financial resources as well as contributing strategic and management experience.

Consolidation and build-ups. As the operating environment gets tougher, the advantages of scale become more obvious. Many industries have become ripe for consolidation. The private equity backed mid-market companies that lead these consolidations will benefit in multiple ways: higher margins through synergies, broader offerings, cross-selling to acquired customers, regional/international expansion and enhanced ability to attract talent.

Secondaries. As well as denominator or portfolio management considerations, there is a structural re-balancing between some traditional institutional private equity investors, such as defined contribution pension plans and insurers, who have achieved their return objectives with private equity. As a result, they are looking to re-allocate to bonds given the more attractive fixed income opportunities that are available now. This will result in attractive secondaries dealflow, ranging from traditional LP stakes to GP-led continuation funds, as well as other structured solutions. How secondaries investors should distinguish between the different opportunities will be a topic in the next quarterly letter.

As has been shown by the SVB collapse, the current environment also brings important risks and challenges that should not be overlooked. A fly on the wall in our investment committee meetings would see that we leave no stone unturned when we consider all possible downside scenarios. With the luxury of a healthy dealflow, we have no qualms in rejecting deals if they do not meet the very high bar required for us to invest. We look forward to reporting on the exciting investments that make the grade.

Yours sincerely,

The Private Equity Investment Team,

Unigestion

Unigestion Private Equity Activity

Here are the highlights of some of the investments that we completed in Q1

In March, we committed to Hg Mercury 4. Hg Capital is one of the Pan European leaders in the mid-market, with a focus on software and services companies along eight clusters: Tax & Accounting, ERP & Payroll, Legal & Regulatory Compliance, Automation & Engineering, Technology Services, Healthcare IT, Capital Markets & Wealth Management IT, and Insurance. The Firm pursues three parallel strategies: Saturn, which invests in upper mid-market companies, Genesis, which invests in mid-market companies and Mercury, which invests in the lower mid-market. Unigestion has previously invested in Hg’s Mercury and Genesis programmes.

Also in March, we committed to Axiom I. Axiom’s investment strategy is to focus on ambitious high growth companies that are too mature for venture capital funds but still fly under the radar of larger UK mid-market funds. To be considered attractive for Axiom, a company has to operate in the UK B2B SaaS market, show 20%-50% growth in (mostly recurring) revenues in the range of GBP 5m – 20m and have a highly sticky mission critical product offering. Its value creation approach is to leverage its big tech network with strong relationships in key areas, implementing its growth hacking team with an operational focus through a high degree of data analytics and supporting the management with its expertise in M&A.

In February, we committed to Charterhouse XI. Charterhouse is a Pan-European manager located in London with 36 investment professionals. Charterhouse targets mid-market companies (typically family-owned businesses) headquartered in western Europe, primarily across services, healthcare, specialised industrials and consumer sectors. Charterhouse XI currently has three investments including a French private higher education platform providing tuition and qualifications to 17,000 students through a network of 21 schools across France, a leading children’s English as an Additional Second Language (“EASL”) provider with 526 schools, and a European Funeral Services and Crematoria business operating in France, Italy, the Netherlands, Germany, Belgium, and Switzerland.

In January, we closed a secondary investment in Capiton Quantum, a multi-asset continuation vehicle. The vehicle includes two well-performing niche companies in the microelectronics and nanofabrication industries. The first company is a full-service provider of advanced packaging for micro- and opto-electronic systems focusing on highly customised, low volume applications with very specific, hire precision requirements. The second company is a global developer and manufacturer of systems and software for the production and analysis of nanofabrication structures. The assets are expected to benefit from long-term growth trends in the global semiconductor market, driven by ongoing digitalisation, increasing demand for connected electronic devices and global innovation mega-trends.

In the same month, we closed a secondary investment in Samara IIB, a multi-asset continuation vehicle. The USD 150m transaction includes three companies from Samara Fund II – a manufacturer of minimally invasive cardiovascular devices (stents, structural heart devices) with market leadership in India and a sales presence across 69 countries; a staffing company in India, offering diversified HR staffing solutions with a headcount of more than 118,000 associates; and a Hyderabad-based biryani chain restaurant with over 70 outlets across 10 cities in India. All three assets are within the top three players in their respective segments and are high quality companies with different underlying growth drivers.

Important information

INFORMATION ONLY FOR YOU

This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

RELIANCE ON UNIGESTION

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time. Such information is intended to provide you with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf of one or more Unigestion entities will be involved in managing any specific client account on behalf of another Unigestion entity.

NOT A RECOMMENDATION OR OFFER

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Reference to specific securities should not be construed as a recommendation to buy or sell such securities and is included for illustration purposes only.

RISKS

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Unigestion maintains the right to delete or modify information without prior notice. The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, and may experience substantial & sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

PAST PERFORMANCE

Past performance is not a reliable indicator of future results, the value of investments, can fall as well as rise, and there is no guarantee that your initial investment will be returned. Returns may increase or decrease as a result of currency fluctuations.

NO INDEPENDENT VERIFICATION OR REPRESENTATION

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

FORWARD-LOOKING STATEMENTS

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events and are subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. You are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

TARGET RETURNS

Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Target returns are based on Unigestion’s analytics including upside, base and downside scenarios and might include, but are not limited to, criteria and assumptions such as macro environment, enterprise value, turnover, EBITDA, debt, financial multiples and cash flows. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

USE OF INDICES

Information about any indices shown herein is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison. You cannot invest directly in an index and the indices represented do not take into account trading commissions and/or other brokerage or custodial costs. The volatility of the indices may be materially different from that of the strategy. In addition, the strategy’s holdings may differ substantially from the securities that comprise the indices shown.

ASSESSMENTS

Unigestion may, based on its internal analysis, make assessments of a company’s future potential as a market leader or other success. There is no guarantee that this will be realised.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of this fund and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.

Legal Entities Disseminating This Document

United Kingdom

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

United States

In the United States, Unigestion is present and offers its services in the United States as Unigestion (US) Ltd, which is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and/or as Unigestion (UK) Ltd., which is registered as an investment advisor with the SEC. All inquiries from investors present in the United States should be directed to clients@unigestion.com. This information is intended only for institutional clients that are qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

European Union

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

Canada

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

Switzerland

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued May 2024.

Related insight

- Corporate

- Press releases

Unigestion has invested in Grupo Gestcompost – a a leading platform in the biogas and biomethane sector in Spain – via its Climate Impact Fund.

[…]- Equities

- Perspectives, Research

In our latest research, we explore a breakthrough approach – leveraging neural networks within a learning-to-rank framework – to enhance stock selection accuracy in increasingly complex markets.

[…]- Corporate

- Press releases

Unigestion has agreed to sell its successful investment in Micronics Engineered Filtration Group (‘Micronics’) to Cleanova and will make a new investment in Cleanova from its sixth secondary vintage.

[…]- Corporate

- Press releases

Unigestion has announced a strategic partnership with Kepler Cheuvreux to establish a joint asset management company specialising in quantitative strategies for public equities.

[…]